Insurance company mathematicians have calculated a method to squeeze millions more in federal subsidies. It’s called Silver Loading………………

There are hidden gems to be found in most federal legislation, especially legislation like the ACA. As House Minority Leader Nancy Pelosi said of the Affordable Care Act, in 2010: “We have to pass the bill so that you can find out what is in it.” The ACA is a prime example. Carriers active in the individual health insurance market place have seized upon something in the ACA that lends itself to innovative mathematical wizardry to squeeze more government subsidies from the national treasury.

The premium subsidy (welfare) tax credits is based on the cost of the benchmark Silver plan…but the subsidies themselves can be applied to ANY plan. The trick is to get more federal tax dollars to fund premiums. The higher the rates for the Silver Plan the more the government subsidizes the cost for all the plans.

How Silver Loading works:

The ACA includes two types of financial subsidies. Advance Premium Tax Credits (APTC) reduce monthly premiums for low- and moderate-income.

Cost Sharing Reductions (CSR), meanwhile, reduce deductibles, co-pays and other out-of-pocket expenses for low-income enrollees.

In 2017, Donald Trump cut off CSR reimbursement payments in a failed attempt to sabotage the ACA, thinking this would cripple the ACA exchanges. Instead, insurance carriers implemented a very smart alternative pricing mechanism to make up for their CSR losses, which came to be known as “Silver Loading.”

The carriers basically calculated how much they expected owe in CSR expenses the following year…and then simply added that amount to their premiums for the following year instead.

While there’s several ways that carriers can add the extra CSR cost to their premiums, “Silver Loading” involves doing so by adding 100% of the extra cost to Silver plans only, as opposed to spreading it out across Bronze, Silver, Gold & Platinum plans.

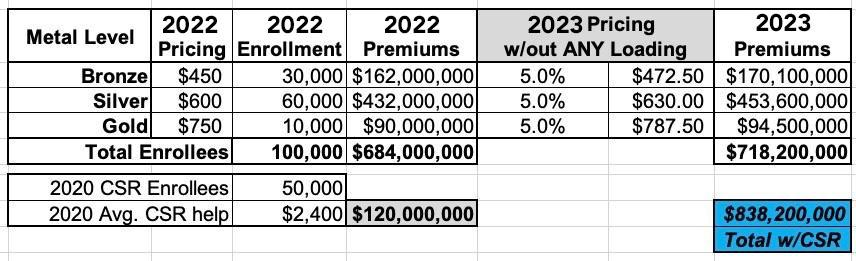

For example:

A carrier thinks overall claims next year will increase by around 5%. To keep things simple, let’s say they offer just 3 plans: One Bronze, one Silver and one Gold, priced at an average of $450, $600 and $750/month.

This carrier has 100,000 enrollees this year and expects to pay out $120 million in CSR assistance. They assume total enrollment and CSR costs will be around the same (and in the same ratios) next year.

They know they aren’t gonna get reimbursed from the federal government for their CSR costs next year, so simply raising their premiums by 5% would mean a $120 million loss. Ouch:

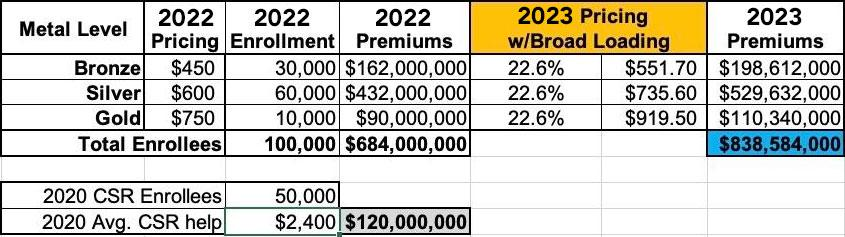

What happens if they load their projected CSR losses evenly onto the premiums instead?

They take the $120 million total and divide it by 12 months ($10 million/mo), then divide that across the projected enrollment for each plan.

If they do it this way, premiums for all three plans would go up by 22.6%. This is known as Broad Loading:

If a carrier Broad Loads (let’s assume, again for simplicity, that one of their Silver plans is also the benchmark Silver that APTC subsidies are based on), then the subsidies also increase by roughly 22.6% to match the premium increase. This makes the net cost of Silver plans for subsidized enrollees roughly the same, Bronze plans slightly less expensive, and Gold plans slightly more expensive than they otherwise would’ve been…because a 22.6% price increase on a larger number is going to be more than the 22.6% premium increase based on the Silver plan.

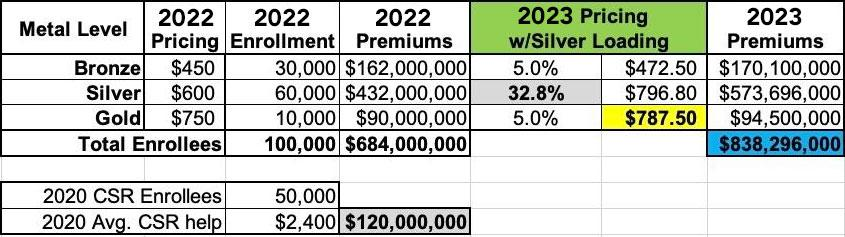

HOWEVER, what happens if you Silver Load instead?

In this case, they tack the full $120M onto the cost of Silver plans only. Bronze & Gold plans go up by 5% while Silver plans jump by 32.8%:

Whether the carrier Broad Loads or Silver Loads, they still end up covering their CSR losses, right?

So what’s the point of Silver Loading?

Well, the key to this is that the formula for the premium subsidy tax credits(APTC) is based on the cost of the benchmark Silver plan…but the subsidies themselves can be applied to ANY plan.

Notice how the Gold plan is now priced LOWER than the Silver plan? That means that an enrollee can now get a Gold plan (which have lower deductibles/other cost sharing) for less than (or around the same as) a Silver plan instead. Even more important, it means that the APTC subsidies are increased, thus making Bronze plans free (or dirt cheap) for many subsidized enrollees…and even some Gold plans.

In fact, last year there were over 600 counties nationwide where many people could get $0-premium Gold plans…in large part thanks to Silver Loading. There are millions of ACA enrollees who earn more than 200% of the Federal Poverty Line who have been saving thousands of dollars since 2018 thanks to this policy.

SOURCE: Texas Republicans pass law which dramatically improves the ACA.