(click on map to enlarge)

Blue Cross and Blue Shield health insurers cover about a third of Americans, through a national network that dates back decades. Now, antitrust lawsuits advancing in a federal court in Alabama allege that the 37 independently owned companies are functioning as an illegal cartel.

Customers, health-care providers accuse insurance network of acting as a cartel

By ANNA WILDE MATHEWS

Updated May 27, 2015 5:06 p.m. ET

Blue Cross and Blue Shield health insurers cover about a third of Americans, through a national network that dates back decades. Now, antitrust lawsuits advancing in a federal court in Alabama allege that the 37 independently owned companies are functioning as an illegal cartel.

A federal judicial panel has consolidated the claims against the insurers into two lawsuits that represent plaintiffs from around the country. One is on behalf of health-care providers and the other is for individual and small-employer customers.

The antitrust suits allege that the insurers are conspiring to divvy up markets and avoid competing against one another, driving up customers’ prices and pushing down the amounts paid to doctors and other health-care providers.

The suits, which name all of the Blue Cross and Blue Shield companies as defendants as well as the Blue Cross Blue Shield Association, have already survived the insurers’ first major legal challenge.

U.S. District Judge R. David Proctor last year declined to dismiss them, saying that the plaintiffs “have alleged a viable market-allocation scheme,” which, if proven, could be an antitrust violation. Judge Proctor also said certain federal antitrust exemptions for the insurance business didn’t appear to apply to the behavior at issue in the lawsuits. The suits have moved into the discovery phase; the plaintiffs are seeking class-action status.

Antitrust experts who aren’t involved in the litigation say the suits pose a high-stakes test for the companies, which have long been at the heart of the American health system. “It is a very big deal,” said Tim Greaney, a professor at Saint Louis University School of Law. “The dollars involved are potentially huge.” He and others say the litigation will take years to resolve, unless a settlement is reached.

Both plaintiff groups have prominent attorneys. The legal team for the health-insurance customers includes David Boies, who represented federal antitrust regulators against Microsoft Corp. Whatley Kallas, a firm that has won high-profile settlements from insurers on behalf of physicians, is helping to lead the provider case.

The Blue Cross and Blue Shield companies trace their roots to the 1930s, when hospital and doctor groups started insurance plans to help people pay for medical care. Hospital plans used the Blue Cross name, and the physician plans were sold under the Blue Shield banner. Eventually, the names were trademarked.

Today, the Blue Cross Blue Shield Association licenses the brands to the insurers that use them. Companies typically hold exclusive rights to the Blue Cross and Blue Shield names within a certain territory.

Most of the 37 Blue Cross and Blue Shield companies are not-for-profit. Many do business in a single state. The biggest Blue Cross and Blue Shield company is publicly traded Anthem Inc., which operates the plans in 14 states. In a few places, Blue-branded plans compete directly against one another, as in California, where Anthem Blue Cross battles Blue Shield of California.

A pair of antitrust lawsuits against Blue Cross and Blue Shield, whose health insurers cover about a third of Americans, have moved into the discovery phase in an Alabama federal court. PHOTO: GERRY BROOME/ASSOCIATED PRESS

The Blue association says its licensing deals simply codify trademark rights that date back decades and “do not constitute an agreement to do anything unlawful.” Federal regulators have long known about the licenses and taken no antitrust action, the insurers said in a court brief. The association also says its arrangements ensure that its members focus on building the Blue brand, and increase competition by helping the Blue companies ally to go up against national insurers.

“This is a model that has withstood scrutiny over our entire history,” said Scott Nehs, general counsel of the Blue association. “There’s no smoky room involved, there’s no dividing up.” Also, he said, the insurers’ rates are closely watched by state regulators.

The plaintiffs, however, allege that the Blue association is controlled by its members, who use it to engage in “illegal market division.” The customer suit says the association also limits the amount of insurance business insurers can do under non-Blue brands. The suit also alleges that the Blue agreements result in “inflated premiums.”

“You have less competition in a market, so prices are higher,” said William Isaacson, an attorney with Boies, Schiller & Flexner LLP, which represents the customer plaintiffs. “That’s one of the basics of antitrust law.”

The suit filed by the health-care providers alleges that because of “decreased competition, health-care providers, including the plaintiffs, are paid much less than they would be” without the Blue association’s agreements. “The fact that someone’s been doing something a long time doesn’t make it right, and doesn’t make it legal,” said Joe Whatley, a lead attorney for the provider plaintiffs. Mr. Whatley declined to say whether there were settlement negotiations under way but said “we are always open” to talks.

The plaintiffs have “some surprisingly strong claims,” said Mark Hall, a professor at Wake Forest University School of Law. “It’s sort of antitrust law 101 that direct competitors can’t agree to divvy up their territory.”

Still, said Scott E. Harrington, a professor at the University of Pennsylvania’s Wharton School, “it’s going to be hard to show those entities are making the large margins implied by” the allegations. The Blue Cross and Blue Shield plans don’t always have big profits, he said.

Glenn Melnick, a professor at the University of Southern California, said the two sets of plaintiffs in the case had diverging interests, because higher payments to health-care providers would likely push up premiums for insurance customers. “They appear to be arguing conflicting outcomes,” he said.

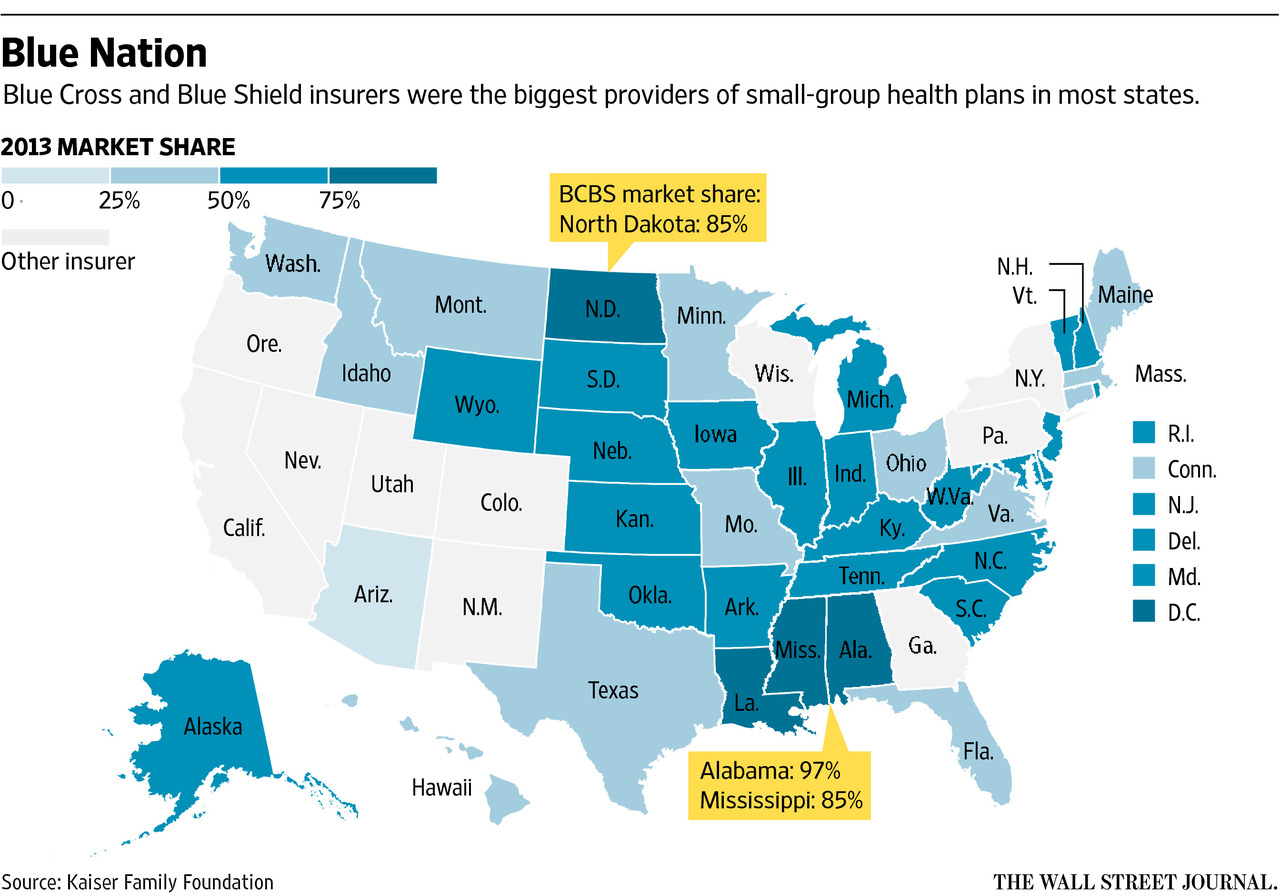

The Blue plans often have significant market share. According to an analysis by the Kaiser Family Foundation, Blue Cross and Blue Shield companies were the biggest players in the vast majority of states’ small-business and individual insurance markets in 2013, the most recent data available. In some states, their share was a commanding one. Blue Cross and Blue Shield of Alabama held 91% of the individual business and 97% of the small-group market in its state.

A spokeswoman for Blue Cross and Blue Shield of Alabama referred questions to the association, which said that the insurer competes with 10 other companies selling commercial health insurance, and that a federal survey showed Alabama has the lowest average family premiums in the U.S. and among the lowest employer premiums.

Ultimately, the antitrust cases may hinge on tensions between the laws governing trademark rights and the antitrust statutes, antitrust experts said. A restaurant operator, for example, can legally license its brand to franchisees, granting each a certain territory. The question is whether the Blue setup is more like a franchising arrangement or if it involves unacceptable agreements between potential rivals, said Barak D. Richman, a professor at Duke University School of Law.

“You’ll be looking for cartel-like behavior or the protection of intellectual property,” he said. “That will probably be the most significant evidentiary test.”

Write to Anna Wilde Mathews at anna.mathews@wsj.com