Milliman White Paper Shows How Self-funding Gives Employers More Control Over Medical Insurance Programs

MyHealthGuide Source: Jennifer Janvrin, CEBS, 11/2018, Milliman White Paper (full text)

Editor’s Note (Ernie Clevenger): This excellent White Paper by Milliman provides key values of self-funded and statistical tables to illustrate risk and risk management.

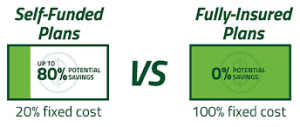

To gain control over the ever-increasing cost of employee health insurance, more and more employers are discontinuing their fully insured coverage and switching to self-funded models. Basically, this is an unbundled approach that separately hires all of the required functions–medical provider networks, carrier or TPA, PBM, stop-loss insurer, and consultants–subject to competitive bidding. Significant cost reductions in the neighborhood of 5% to 10% are typical.

Of equal concern to employers are quality and administrative efficiency. In many cases, quality remains unchanged because self-funded programs are able to retain the exact same medical networks and coverages offered previously. The transition happens seamlessly behind the scenes, so that employees are not even aware of it.

Key benefits of self-funding:

- Net expense reduction

- Enhanced cost-benefit insight into every aspect of the program

- Flexible plan design

- Total access to claims data

- Control of paying claims and investment income on reserves

Below is a quick overview of the actuarial parts of the program: estimating claims for the coming year, setting the employer’s budget, evaluating risk tolerance, and planning the strategy for stop-loss coverage.

Expense reduction

Annual premium increases under a fully insured arrangement are not only due to rising costs related to healthcare claims. A significant portion of the total premium is from taxes and mandated fees, which typically increase proportionately to the rising healthcare claims costs.

For 2017, fully insured employers enjoyed a “relief year” from fees imposed by the Patient Protection and Affordable Care Act (ACA); 2019 will also be a “relief year” from these fees. However, in 2018, according to what we have seen, an insurer fee of approximately 3.9% of premiums has been added to the employer’s burden. This percentage is anticipated to be even higher in 2020, after the 2019 “relief year.” This will be in addition to the premium tax of approximately 2%.

Of course insurers are in business to make money, and their profit and risk margins add an invisible layer of fees to your healthcare expenses. The combination of the insurer’s margins and premium tax, combined with the insurer fee, can add up to 5% to 10% to your total premium. That amount is part of the potential savings employers can realize by switching to self-funded programs. In addition, shopping the market can result in further savings on claims administration fees and stop-loss premiums.

Enhanced insight

Self-funded programs carry fees and expenses too. That’s why the first step for an employer is to evaluate a detailed feasibility study, prepared by an independent third party with consultants knowledgeable in this field. The analysis should provide a clear look at how a self-insured arrangement compares to a fully insured one, and should include a detailed comparison of projected claims and expenses under both arrangements.

To estimate claims costs, data such as historical medical and prescription drug claims, large claims, participant enrollment information, plan design changes over previous plan years, and historical enrollment shifts in those plans is gathered and projected to a given time period. Any significant changes in networks and in the demographic profile of the covered population would be considered in order to make the projection as accurate as possible for the population that may be self-funded. If the group size is not large enough, or historical data is unavailable or limited, an expected claims cost will need to be estimated utilizing the group’s demographics. This type of expected claims cost is typically called a manual rate.

A confidence level, technically described as “credibility,” is calculated for the manual rate based on the size of the group and how much historical claims data is available. A guideline for “credibility to manual” is shown in Figure 1.

| FIGURE 1: CREDIBILITY TO MANUAL | |||

| NUMBER OF MONTHS OF HISTORICAL CLAIMS DATA | |||

| NUMBER OF EMPLOYEES | 0-12 | 13-24 | 25+ |

| 50-79 | 95.0% | 85.0% | 70.0% |

| 80-99 | 85.0% | 72.5% | 60.0% |

| 100-149 | 80.0% | 65.0% | 50.0% |

| 150-224 | 70.0% | 52.5% | 35.0% |

| 225-299 | 55.0% | 50.0% | 25.0% |

| 300-399 | 40.0% | 25.0% | 10.0% |

| 400-499 | 20.0% | 10.0% | 0.0% |

| 500-749 | 5.0% | 2.5% | 0.0% |

The study will also evaluate differences in fees under fully insured and self-insured arrangements. For a fully insured arrangement, the administration fees, pooling charge, carrier margin, and premium tax will need to be incorporated along with the insurer fee if it is applicable for the projection period. Fees under a self-insured arrangement will include fees for administration of the plan and stop-loss coverage premiums.

They will not include the fully insured carrier’s margin, premium tax, and the insurer fee. In the study, if actual fees are not available then fees would be estimated based on what the employer will typically be expected to see for its market.

The first line of Figure 2 shows the expected claims cost estimate for a sample employer group on a per employee per month (PEPM) basis. The lower section of Figure 2, titled “Expenses (PEPM),” breaks down all of the fees expected to be added to the actual medical and prescription drug costs to arrive at the full cost of coverage. The table itemizes each cost for both the current fully insured solution and the self-funded approach. For the fully insured solution, you can see the impacts of the premium tax and insurer fee that was mentioned in the previous section–along with all of the other line items that apply.

| FIGURE 2: SIMPLIFIED EXAMPLE OF FEASIBILITY STUDY | ||

| FUNDING ARRANGEMENT | ||

| FULLY INSURED |

SELF- INSURED |

|

| EXPECTED CLAIMS COST (PEPM) | $782.02 | $782.02 |

| EXPENSES (PEPM) | ||

| CLAIMS ADMINISTRATION & MARGIN | $99.04 | |

| POOLING CHARGE | $84.44 | |

| PREMIUM TAX | $20.85 | |

| INSURER FEE | $40.66 | |

| PCORI FEE | $0.50 | $0.50 |

| CONSULTING FEES | $15.00 | $15.00 |

| CLAIMS ADMINISTRATION | 38.19 | |

| PBM FEE | $1.10 | |

| ACCESS FEE | $7.05 | |

| INDIVIDUAL STOP-LOSS PREMIUM | $74.19 | |

| AGGREGATE STOP-LOSS PREMIUM | $5.36 | |

| TOTAL EXPENSES | $260.49 | $141.39 |

| PROJECTED CLAIMS AND EXPENSES | $1,042.51 | $923.41 |

There is a different set of expense items for the self-funded solution. The premium tax and insurer fee are gone–they no longer apply. Oftentimes, with a fully insured carrier, full transparency on the amount of fees you are paying is not available. This is another important benefit of self-insuring. Full transparency of the underlying costs allows you to analyze the value received for each part of the program.

Flexible plan design

Insurers offer a variety of plans that meet employers’ needs reasonably well. But are they a perfect fit? With a self-funded plan, employers can design every aspect of the program. There are no state-mandated benefits, so it’s really up to you to decide which coverages will work best for your employee population.

You can select a broad or narrow network, design a program with multiple service tiers, implement a high-deductible plan, and offer wellness and disease management programs.

Or you can choose to replicate the networks and coverages from your existing fully insured program. Your broker can recommend providers with the appropriate capabilities and work with them to tailor their offerings to your specifications.

Access to data

In a fully insured plan, the carrier receives all of the claims and processes the data. They typically issue reports on a fixed schedule using their standard reports such as premium versus claims or monthly incurred claims. This arrangement is inadequate for an employer that would like more insight into the population’s experience. A self-funded employer will likely want to analyze and model different scenarios to determine how well its benefit strategy is working.

Self-funded programs can be designed to address your specific data requirements. Typically, self-funded employers’ claims data is available through an online portal that allows you to access the data whenever you want. Also, the data presented can be tailored to match your desired criteria. For example, maybe you’d like to examine the claims experience of a new high-deductible plan, or to compare outcomes of people in your wellness plan with those who don’t participate in the wellness plan. Working with your consultant so they understand your needs is an important step in properly setting up the data structure with the TPA or carrier. When implemented properly, your reports will be readily available in a form and format that present the exact information you want to see and how you want to see it.

Puts you in control

While cost savings in regard to fees may be paramount, the intrinsic value of a self-funded program is the way it puts the employer in control of paying its own claims and reserving for those claims. In a self-funded plan, funds are held in a reserve account until bills for medical claims become due. Employers can capture investment income earned on these reserves. Under a fully insured arrangement, with each monthly premium you are paying in advance for medical treatment that typically has not yet been delivered. The insurer has those dollars and potentially does not have to pay them out until months later, when the medical providers’ bills come due. These dollars could be described as “the float.” Thus, the insurer is able to earn investment income on “the float” instead of the employer earning this investment income and being in control of its cash flow.

It is important to note that even though an employer has more control of its cash flow it also has to deal with claims volatility versus just paying a set premium to a carrier. The amount of risk around this volatility that an employer is willing to tolerate needs to be evaluated in making the decision to self-insure.

Stop-loss strategies

Risk management is critical to the success of any self-funded medical insurance program. Under the fully insured model, if your employees’ medical claims in a given year exceed the amounts covered by the premiums, the insurance carrier would absorb that additional cost. By insuring thousands or millions of employees working at hundreds of companies, insurers are able to reduce total claims volatility and diversify the risk associated with catastrophic events.

Obviously, a single company typically does not have this ability to diversify its risks. Instead, self- funded insurance programs must effectively manage their risks. First, it is advisable to evaluate the probability of exceeding each year’s total estimated claims cost.

It may be part of a company’s risk strategy to add a cushion to each year’s expected medical costs. For example, to satisfy an employer’s level of risk tolerance, it might be necessary to set aside reserves that accumulate from budgeting at 105% to 125% of expected costs.

Figure 3 presents three different-sized employer groups with the same PEPM claims costs. The example shows the probability these employers have of exceeding expected claims costs.

Statistically it makes sense for smaller groups to have a lower tolerance for risk. Higher claims volatility is more evident with their smaller numbers of members and a few expensive medical problems can cause the plan’s actual cost to exceed expectations.

| FIGURE 3: ASSESSING APPROPRIATE BUDGET LEVELS | ||||||||||||||||||

| Analysis of Aggregate Claim Variability | ||||||||||||||||||

| 35% | 32.6% | |||||||||||||||||

| 30% | 26.7% | |||||||||||||||||

| 25% | 22.4% | |||||||||||||||||

| 20% | ||||||||||||||||||

| 15% | ||||||||||||||||||

| 10% | 10.5% | |||||||||||||||||

| 5% | 2.3% | 4.3% | 1.6% | |||||||||||||||

| 0% | 0.2% | ~0.0% | ||||||||||||||||

| % of Expected | 105% | 115% | 125% | 105% | 115% | 125% | 105% | 115% | 125% | |||||||||

| 200 Employees/ 488 Members $75,000 individual Stop-loss |

500 Employees/ 1,200 Members $125,000 individual Stop-loss |

1,000 Employees/ 2,439 Members $200,000 individual Stop-loss |

||||||||||||||||

| FIGURE 4: CHOOSING THE RIGHT DEDUCTIBLE FOR INDIVIDUAL STOPLOSS COVERAGE | ||||||||||||||||||

| Analysis of Individual Claim Variability | ||||||||||||||||||

| Spec Deductible | $50K | $75K | $100K | $100K | $125K | $150K | $150K | $200K | $300K | |||||||||

| 95th Percentile | 9.0 | 6.0 | 4.0 | 8.0 | 6.0 | 5.0 | 8.0 | 5.0 | 3.0 | |||||||||

| Expected | 5.4 | 3.0 | 1.7 | 4.2 | 3.0 | 2.2 | 4.3 | 2.6 | 1.3 | |||||||||

| 25th Percentile | 4.0 | 3.0 | 1.0 | 3.0 | 2.0 | 1.0 | 3.0 | 1.0 | 0.0 | |||||||||

Figure 4 presents recommended level of individual stop-loss coverage for each plan, as well as the number of individual claims these employers would typically experience at each deductible level.

Figure 4 demonstrates how the greater the head count is, the higher the deductible can be set and still achieve approximately equivalent risk control. Looking more closely at Figure 4, we can see the stop-loss level needed to keep claims at a reasonable level will vary by employer size: A company insuring 200 employees might choose an individual stop-loss level of $75,000.

This stop-loss amount tends to approach $125,000 as employee counts near 500. And $150,000 to $300,000 works well for groups closer to 1,000 employees.

Another tool to manage risk is aggregate stop-loss coverage. It pays for total claims in excess of a contracted amount called the attachment point. Typically, the stop-loss insurer would set the attachment point at 125% of expected claims. The insurer would then be responsible for paying all claims–in aggregate—over that amount.

Aggregate stop-loss coverage is a risk-management approach that is similar to being fully insured. If an employer budgets at the stop-loss contract’s attachment point it will have a 0% chance of exceeding its budget. While the coverage is inexpensive in simple dollars terms, it is quite expensive relative to the low probability of reimbursement that actually occurs. In most cases, a well-designed individual stop-loss strategy, along with an adequate estimate of expected claims, meets the employer’s risk management requirement.

Smaller groups will have a higher need for aggregate stop-loss than larger groups. The 125% threshold is labeled for the various-sized employer groups. Based on Monte Carlo simulations, there’s only a 2.3% chance of exceeding a 125% attachment point for a 200-member group and an approximately 0% chance of exceeding 125% for a 1,000member group. This assumes these groups have similar expected claims costs that were set appropriately and similar demographics.

This translates to one reimbursement every 43 years for the smaller group. Other variables in the health care system may alter these results and it is important to be aware of these other factors.

Often employers closer to the 200-covered-employees range will opt for this coverage in the first year of the transition to self funding. Once they get used to the process and the claims experience of their groups, they more often than not dispense with aggregate coverage.

Next steps

Self-funding is a great solution for managing the rising cost of insurance premiums, which, as noted above, is partly driven by increased taxes and fees. That said, self-funding may not be appropriate for every business. You should determine whether all of the providers and networks that you want to offer your employees will be available to the new program. You should also compare all costs under a self-insured versus a fully insured arrangement.

A fully insured quote may be available at a lower cost than what a self-funded approach may cost. It’s important to work through a detailed feasibility study to fully understand the cost savings that may be available. And, most importantly, would self funding fit within your company’s tolerance for risk, and how is your company going to manage that risk?

Today, more and more companies, with employee populations as low as 100, are finding that self-funding makes economic sense and enhances their control over this important benefit. As such, it is certainly worth your while to align yourself with a strategic partner who can show you options based on your specific situation, and help you transition to a self-funded arrangement if that is what you choose to pursue.

About Milliman

Milliman is among the world’s largest providers of actuarial and related products and services. The firm has consulting practices in life insurance and financial services, property & casualty insurance, healthcare, and employee benefits. Founded in 1947, Milliman is an independent firm with offices in major cities around the globe. Visit milliman.com–