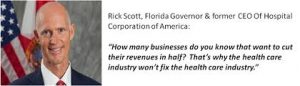

The following article illustrates the angst hospitals are undergoing in defending their indefensible and egregious pricing strategies through their PPO collaborators. The solution posed in this article by a hospital advocate is: Identify Reference Based Pricing (RBP) patients and don’t treat them! But that short sighted response brings on Cash Pricing strategies through companies like Asserta Health (www.assertahealth.com) which often times saves plan sponsors even more money than otherwise would have been paid hospitals under a typical RBP plan. Making lemonade out of lemons……………

Article Contributed By John Powers, AMPS

Responding to Non-Network Plans Using Reference-Based Pricing

Hall Render Killian Heath & Lyman PC

USA September 20 2016

An increasing number of employer-sponsored health plans are electing not to enter into contractual agreements with hospitals through an established provider network. These plans seek to limit payment for hospital services provided to plan beneficiaries by repricing the services at a plan-determined amount, typically based upon a percentage of Medicare reimbursement, an amount far below traditional commercial payment for the same services.

Generally, a hospital is not required to discount its charges absent a written agreement. These plans often attempt to create the appearance of an agreement by including language on plan identification cards, EOBs and other documents stating that by agreeing to accept assignment of payment from the plan, a hospital also agrees to accept the plan-determined amount as payment in full. If the hospital balance bills the patient for the outstanding balance, the plan will assign legal counsel to vigorously defend the plan’s action. Regardless of the ultimate outcome, the patient is placed in the middle of a dispute between the hospital and the plan.

It is important for hospitals to proactively respond to these tactics by managing expectations in a clear and consistent manner. As early as possible, hospitals need to inform both the plan and the beneficiary that the hospital does not agree to discount billed charges, absent a written agreement to do so, and without such an agreement, the beneficiary may be responsible for any shortfall between the hospital’s billed charges and plan benefits.

Details

Medical benefit consulting firms (“Re-Pricers”) are causing a commotion in many states by telling employers they may dictate the amount an employee health plan (“Plan”) will pay for hospital services. Typically, the Plan document provides coverage only for “Allowable Claim Limits,” and the Plan delegates to the Re-Pricer its authority to review, audit and resolve disputes concerning hospital claims to the Re-Pricer.

“Allowable Claim Limits” are usually based upon a percentage of industry resource(s). For example, Allowable Claim Limits for inpatient services are based upon a percentage of Medicare Reimbursement or a percentage of the hospital’s cost, as reported to CMS on the most recent Medicare Cost Report. Allowable Claim Limits for ambulatory surgical centers are based upon a percentage of the Medicare fee schedule for like services in the geographic area. If there is no Medicare pricing for a service, Re-Pricers will rely upon other published fee and cost lists that provide (in the Re-Pricer’s opinion) a basis for its determination of the reasonable expense for the service.

Because these Plans have no contracted provider network, Plan beneficiaries may elect to obtain services from almost any hospital. The only contractual agreement concerning payment for hospital services is typically in the form of an acknowledgement of financial responsibility signed by the beneficiary during the patient registration process. Therefore, the only remedy for a Plan’s deficient payment is for the hospital to collect the balance from the patient.

Re-Pricers employ a number of tactics intended to obligate a hospital to step into the shoes of the beneficiary and limit the hospital’s remedies to those available under the Plan document. Often the Plan includes language on the back of beneficiary identification cards that purports to restrict hospital charges to the amount the Plan deems reasonable and states that by accepting an assignment of benefits from the beneficiary, a hospital waives any right to recover payment in excess of the Plan-determined Allowable Claim Limit. The explanation of benefits will reflect an adjustment for any billings that exceed the Allowable Claim Limit. Plan beneficiaries are instructed to pay the hospital only the co-insurance and deductible amounts calculated by the Re-Pricer and to contact the Re-Pricer upon the receipt of any balance billing from the hospital or a collection firm. Upon receiving such notification, the Re-Pricer promptly assigns legal counsel to aggressively defend any collection actions. Legal counsel typically sends a form letter in which it demands that the hospital cease and desist all collection activity against the beneficiary and demands that the hospital appeal the determination through the Plan’s internal dispute resolution process.

However, if the hospital assumes the beneficiary’s rights under the Plan, it also accepts the limitations of the Plan coverage. Because the beneficiary is entitled only to benefits in the allowed amount as determined by the Plan, the hospital is left to defend the “reasonableness” of the Re-Pricer’s determination – a decision over which they had no participation, influence or control. Therefore, we generally do not recommend that hospitals pursue an appeal through the Plan. Unfortunately, a hospital’s other options are typically limited to: (i) pursuing a claim against the beneficiary; or (ii) accepting payment in the Allowable Claim Limit amount.

Practical Takeaways

We suggest hospitals develop a strategy to proactively preserve all rights to collect payment in accordance with their own contractual agreements and policies. This strategy begins by reviewing internal registration and collection practices in order to increase early awareness of a potential payment issue and appropriately respond by:

- Ensuring that a patient’s written acknowledgement of responsibility for payment is sufficient to preserve the hospital’s right to pursue a balanced billing action if needed;

- Educating hospital registrars and other front line personnel to look for red flags in beneficiary identification cards;

- Establishing internal processes to track non-network Plans using reference-based pricing tactics;

- Notifying non-network Plan sponsors and beneficiaries that, absent a written agreement signed by an authorized hospital representative: (i) the hospital does not recognize or participate in Plan; and (ii) the hospital will pursue payment for services rendered to beneficiaries in accordance with the hospital’s policies; and

- Establishing a strategy for consistent response to payment reductions by non-network Plans.

We anticipate that Re-Pricers will become increasingly aggressive in response to the dynamic landscape of health care reimbursement. Therefore, hospitals should be vigilant in recognizing their strategies and work with their counsel to develop internal processes for response.

Hall Render Killian Heath & Lyman PC – Angela Smith