“It’s evident that many brokers believe the (PPO) networks are not the long-term answer, but brokers and consultants continue to push business to the traditional model or utilize TPAs with carrier or independent networks because it’s the status quo, what we have always done.”

These are Me Too brokers. “If you like it, I do too. If you don’t like neither to I!” The motivation to “go along to get along” stems from greed and fear of being fired while knowing all along you’re not serving the client’s best interests. A client that stops taking your advice is not one worth keeping. As difficult as it may seem to those living in the Me Too world, firing an errant client is cleansing. And it’s the right thing to do. – Bill Rusteberg

———————————————————–

Are carriers and PPO networks slowly becoming obsolete?

Employers are voicing their concerns over the rising claims and admin costs of their health plans and brokers and consultants are constantly on the lookout for new ideas that can make an impact and help them stay ahead of their competition.

By Mark Hatcher | May 16, 2019 at 08:06 AM

During my 28 years in the employee benefit industry, health insurance has gone through many changes. I have experienced traditional non-network insurance with deductibles as low as $250, HMO and PPO networks, copays for physicians, ER and urgent care, HSAs, FSAs, HRAs and health care reform. And all came about in an attempt to help control health care costs in employers’ self-funded medical plans.

As the HMO and PPO networks still exist with major insurance carriers and the PPO networks with independent networks, they do not offer the savings they were designed for when first introduced to the market over 25 years ago. These networks feature non-transparent agreements with physicians, hospitals and other vendors for reimbursements that, in most cases, still have the insured being balance billed because the difference between the agreed reimbursement amount with the carrier or network is different from the retail price charged by the provider.

We are slowly entering a new era where employers are demanding new ideas and solutions to reduce claims costs and stop loss premiums. The days of the PPO and HMO networks are slowly becoming as obsolete as the rotary phone, because the current system is just not working.

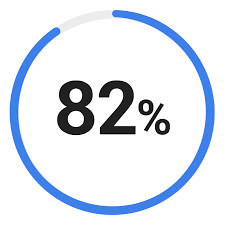

A one-question survey was sent to 300 employee benefit brokers, consultants and account managers in March 2019. The question: “Do you feel as though carrier and independent PPO networks are not saving the claims dollars on covered benefits outside of a physicians office visit?” The results showed that 82 percent said “yes.” It’s evident that many brokers believe the networks are not the long-term answer, but brokers and consultants continue to push business to the traditional model or utilize TPAs with carrier or independent networks because it’s the status quo, what we have always done.

A one-question survey was sent to 300 employee benefit brokers, consultants and account managers in March 2019. The question: “Do you feel as though carrier and independent PPO networks are not saving the claims dollars on covered benefits outside of a physicians office visit?” The results showed that 82 percent said “yes.” It’s evident that many brokers believe the networks are not the long-term answer, but brokers and consultants continue to push business to the traditional model or utilize TPAs with carrier or independent networks because it’s the status quo, what we have always done.

Based on President Trump’s persistency and determination to undo Obamacare, we are bound to see some amount of change before he leaves office, whether after one term or in six years. The free market approach to health care is continuing to come to light and is being brought to market by cost containment vendors that are negotiating with hospitals, out-patient surgery centers, imaging facilities, and cancer and oncology centers, to accept fee schedules in the range of 125 percent to 150 percent of Medicare. This is going to become the new norm, providing competition in the marketplace and controlling costs.

The problem is that no carrier or independent PPO network is going to allow all these cost containment vendors to replace their vendors or change their agreed reimbursements. They might allow, say, the carve-out of dialysis or organ transplant vendors, but not all of them. Self-funded plans in today’s environment need to do something different that will help reduce claims costs and stop loss premiums. The only way to do this is through reference-based pricing and opening the market to allow all cost containment vendors to provide insureds with another option. When designed correctly, these strategies will have zero out of pocket cost to the insured when using one of the direct contract vendors. The incentive is to waive any deductible or out of pocket cost to the insured. By utilizing a cost containment vendor, the savings in the claim will be 30 percent to 80 percent, based on procedure versus the traditional PPO network. Because of the negotiated arrangements with these different vendors, there’s no balance billing like there would be in most PPO network plans.

Related: Balance-billing court cases force hospitals to justify charges Here’s an example of how this works: How do most people deal with health care? Our first move is either to go to our PCP or specialist in the network or, in case of emergency, the urgent care or hospital. From that point, the issue is resolved at the facility or you are referred to go somewhere else, right? We have all been taught that the physician is always right; therefore, we are going to do what they say, right? I’m afraid that if a physician told an insured that the way to fix what ails you is to go home, climb on your roof and belly flop into their front yard, 30 percent might just do it.

But physicians may not always be right. Therefore, there must be a way for insureds to easily have alternatives that will provide the same or better care and that will waive their deductible or coinsurance.

The key to building this successful model with employers is simple: First, remove the PPO network. At the end of the day, the only network that needs to exist is a physicians-only network. Why? Well, he physician is usually the first stop in non-emergency situations and from there, the patients are referred to the next physician or facility.

Second, include multiple cost containment vendors that can provide savings of 30 percent or more in the following high spend areas: surgeries, imaging, lab, durable medical equipment, dialysis and diabetic supplies, organ transplant, cancer and oncology, to name a few. Third, wrap the plan with reference-based pricing so services will be negotiated up front, except for emergencies, at 150 percent to 180 percent of Medicare.

Fourth, don’t rely solely on education in a group meeting or when speaking to new hires. As we all know, employees and dependents will not remember six months into the plan year and will just go and do what their physician tells them. Rather, provide those things but add concierge care to the program. On the back of an insureds medical card, require that all services outside of a PCP or specialist require insureds to call and pre-authorize with a concierge member that can redirect them and provide the option or options to a cost containment member and the incentive of no out of pocket cost should they choose that direction. It’s second opinion in the best form.

Employers are voicing their concerns over the rising claims and admin costs of their health plans and brokers and consultants are constantly on the lookout for new ideas that can make an impact and help them stay ahead of their competition.

When you can provide the same or better care, no out of pocket expense, and zero balance billing, it’s the win-win we all try to strive to achieve in all forms of our lives. And it’s going to change the mindset of how we purchase our medical care going forward.

Mark Hatcher, VP of the Southwest Region for IBA (International Benefits Administrators) has been in the employee benefits space for over 28 years. Mr. Hatcher spent most of his career as an employee benefits broker and consultant before transitioning into the self-funded TPA space.