Medical insurance directly causes price hyperinflation, because it insulates the patient from the financial impact of their medical care decisions…………………

Medical insurance directly causes price hyperinflation, because it insulates the patient from the financial impact of their medical care decisions…………………

What Causes Hyperinflation for Medical Costs in the US? Medical Insurance, Which Is the Problem, Not the Solution

Medical insurance is the main cause of ballooning medical prices, and forcing people to buy it only compounds the problem.

by Mark J. Perry

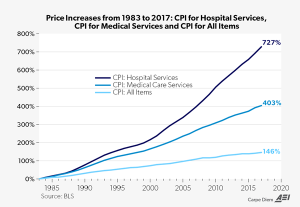

The chart above shows the percentage increases between 1983 and 2017 for: a) the CPI for Hospital and Related Services (+727 percent), b) the CPI for Medical Care Services (+403 percent), and c) the CPI for All Items (+146 percent). Therefore, the price of medical care has increased almost three times more than consumer prices in general, and the price of hospital services has increased about five times more than overall inflation over the last 34 years.

Except for college tuition and college textbooks, there has been no consumer product, good, or service that has increased over time as much as medical care services and and hospital services, to the point that Dr. John Hunt—pediatrician, pulmonologist, immunologist, former academic, former U.S. Navy doctor, inventor, and entrepreneur—calls those medical price increases “hyperinflation.” In an article titled “Health Insurance Is the Problem, Not the Solution” Dr. Hunt explains what causes such price hyperinflation in the medical industry—medical insurance.

Medical insurance directly causes price hyperinflation, because it insulates the patient from the financial impact of their medical care decisions. Above the annual deductible, it’s not the patient’s money. It’s the insurance company’s. The health insurance company is the enemy, hated by the patient for being so expensive and intruding on their doctor’s decisions. Plus the patient isn’t feeling well. So, at best, the patient doesn’t care about the prices (and doesn’t even ask the price). At worst, the patient actively wants to spend the insurance company’s money.

This problem is called a moral hazard and is very well known in the insurance world. I call it the “third-party payer problem.” It affects every decision you make and has ruptured the integrity of everyone involved.

The insured patient doesn’t care about the price of medical care. The doctors are entirely oblivious to the price. (Just try to ask the average doctor what a procedure or a clinic visit costs: few, or none, will have a clue.) So the two people engaged in the transaction—the doctor and the patient—either don’t care about the price or are oblivious to it. You might be forgiven for thinking that at least the insurance companies would want lower prices. But here’s the trick: In our political medical system, the insurance companies actually want higher list prices for medical care!

First, remember that no insurance company pays the list price, ever. Second, the higher the list prices for medical care, the more people feel compelled to obtain the insurance to protect them from the painfully hyper-inflated prices. And third, the high prices of medical care prompt politicians—in their infinite ability to screw things up—to do inane things like unconstitutionally force all Americans to buy the same financial products (“health insurance”) that caused the problems in the first place. And insurance companies—like all cronies—love it when politicians mandate the purchase of their crappy products.

So all three parties in the transaction—the doctor (provider), the patient (customer), and the insurance company (third-party payer)—ALL either want the list prices to be higher, or don’t give a d*** about the price at all. And so the clinic and hospital administrators take the invitation and raise the list prices for services. And nobody fights it—not the busy doctors, nor the patients.

And this is why we have price hyperinflation. The prices, not the costs, of medical care have soared because of this distorted system of medical expense financing known as the third-party payer system. (Don’t believe for a second that the high prices are because of high-tech medical care. It’s a lie. High-tech increases productivity and lowers costs everywhere.)

Unfortunately, the “uninsured” patient gets nailed by the hyper-inflated list prices, with little power to negotiate them down. And so they either avoid their needed medical care because the prices are too high, or they buy into the insurance scam that caused the hyper-inflated prices in the first place.

Insurance is the problem, not the solution.

And what is the solution to rising health care costs? What else, but more free market medicine.

MediBid has doctors all over the country who bid in an auction format to get you the best prices. Check out doctors who practice Direct Primary Care (DPC): for a low monthly fee, DPC docs handle 80% of medical needs and many are available to you 24/7. DPC has made concierge medicine available to the average Joe.

Indeed, there is a small, but growing, set of free market resources out there for patients to use. One would think that free markets in America would be the default. In the medical system, free markets are a remote, but growing, fringe.

Reprinted from American Enterprise Institute.

Mark J. Perry is a scholar at the American Enterprise Institute and a professor of economics and finance at the University of Michigan’s Flint campus.